Juniper Hotels: Did you miss it? Should you buy it?

Juniper Hotels: Did you miss it? Should you buy it?

A Bullish Outlook on Promising Prospects Ahead

In the realm of hospitality investments, Juniper Hotels Limited has recently made a splash with its successful IPO debut, listing at ₹365 per share. This significant milestone not only marks a new chapter for the company but also signals promising prospects ahead. As avid proponents of prudent investment strategies, we are bullish on Juniper Hotels' trajectory and foresee several key factors that contribute to its favorable outlook in the coming years.

Strategic Utilization of IPO Proceeds

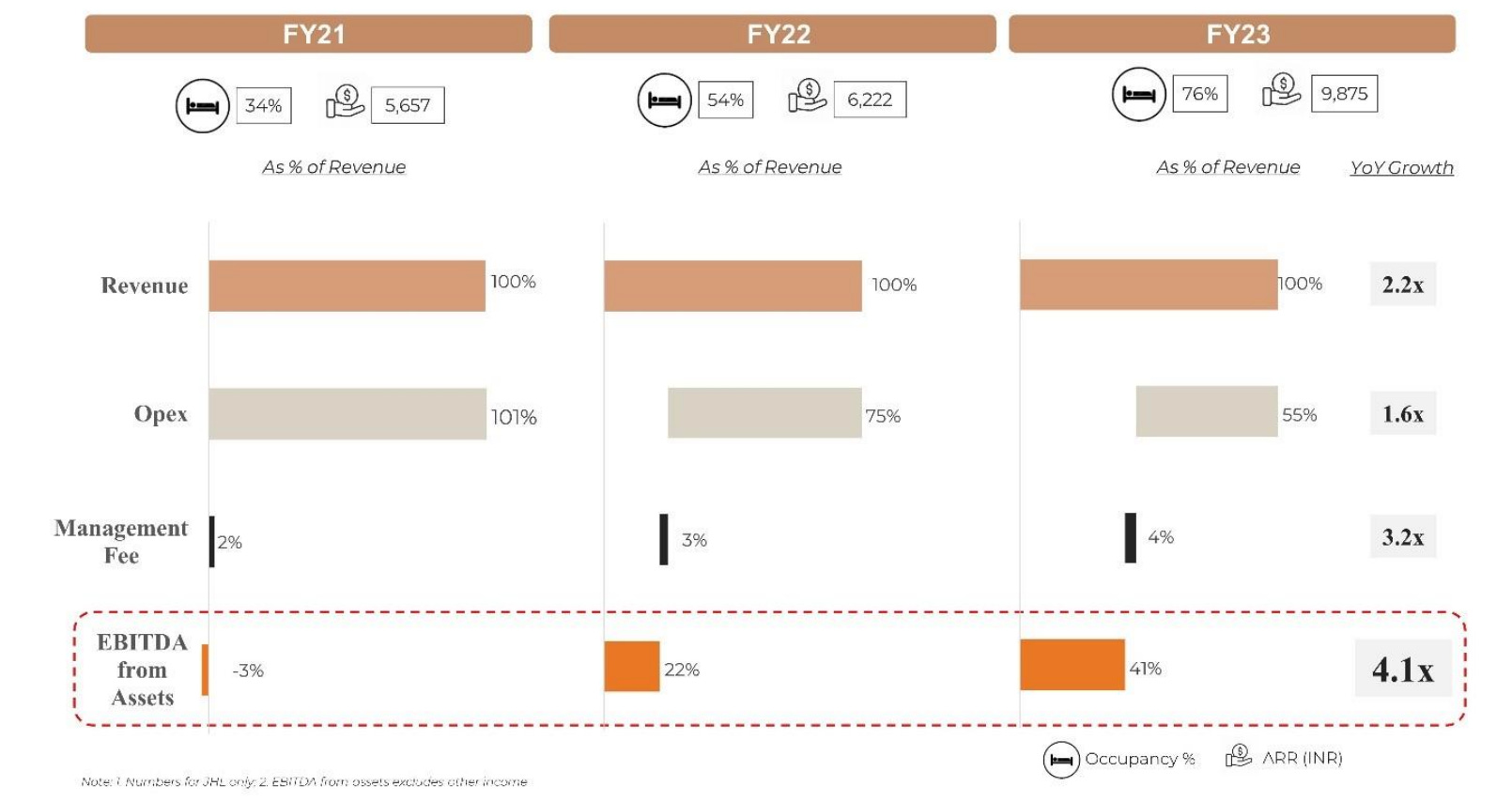

Juniper Hotels intends to utilize the IPO proceeds amounting to ₹1300 crore for debt clearance. This strategic move is poised to have a profound impact on the company's financial health, particularly in terms of interest cost reduction. By clearing a substantial portion of its debt, Juniper Hotels anticipates cutting its interest costs by half. This significant financial maneuver is estimated to add a substantial ₹100 crore to the company's bottom line, thereby bolstering its profitability and enhancing shareholder value.

Promoter Holding and Regulatory Compliance

A noteworthy aspect of Juniper Hotels' post-IPO landscape is the steadfast commitment of its promoters, who currently hold a commanding 78% stake in the company. According to regulatory mandates, this promoter holding is expected to be trimmed down to 65% within a span of three years. It's worth highlighting that historical data suggests a positive correlation between higher promoter holding and favorable stock price performance post-listing. As promoters list the company while retaining a significant ownership stake, it instills confidence among investors, often translating into shareholder rewards through stock price appreciation.